2,633

Views

2,633

Views

0 Comments

0 CommentsAccording to some experts, miners will always be essential to the Bitcoin ecosystem, even after mining the last coins.

Satoshi Nakamoto mined the genesis block on Jan. 3, 2009, minting the first 50 Bitcoin in history and kicking off what would become a billion-dollar industry centered around mining crypto. However, with a cap on Bitcoin supply, the fate of miners after the last coins are issued is unclear.

Bitcoin is created through mining, a process involving computer hardware to solve complex mathematical problems and verify transactions on the blockchain network. For their efforts, miners are rewarded with a predetermined amount of BTC for each block of transactions.

According to the Blockchain Council, more than 19 million BTC has been awarded to miners in block rewards, and according to Nakamoto’s white paper, only 21 million are available. Once this cap is reached, miners will no longer receive rewards for verifying transactions.

Speaking to Cointelegraph, Nick Hansen, founder and CEO of Bitcoin mining firm Luxor Mining, says that despite the loss of block rewards, miners will continue to play an essential role in verifying and recording transactions on the blockchain, but how they are compensated will evolve.

Currently, successfully validating a new block on the blockchain rewards miners with 6.25 BTC, worth about $188,381 at the time of writing, according to CoinGecko. Miners also receive transaction fees.

According to calculations shared in a May 1 tweet from on-chain analytics firm Glassnode, since 2010, fees and block rewards have netted miners over $50 billion.

Since #Bitcoin's inception, Miners have earnt a total revenue of $50.2B from the block subsidy and fees, for an all-time estimated input cost of $36.6B.

This places the all-time-aggregate profit margin for Miners at $13.6B (+37%). pic.twitter.com/TYvBSZbsRo

— glassnode (@glassnode) May 2, 2023

Hansen believes transaction fees will eventually become the primary incentive for miners to continue long after the last BTC is mined.

“That’s why as transaction fees become an increasingly important part of Bitcoin mining economics, understanding transaction fee dynamics and forecasting them into the future becomes even more critical,” he said, adding:

“Thus, it’s important to see fees increase over time, something that Bitcoin Ordinals, as of late, has helped with, for example.”

However, this shift is still likely years away, given that nobody currently mining will be alive when the last BTC block reward is received.

It will be a long wait to find out

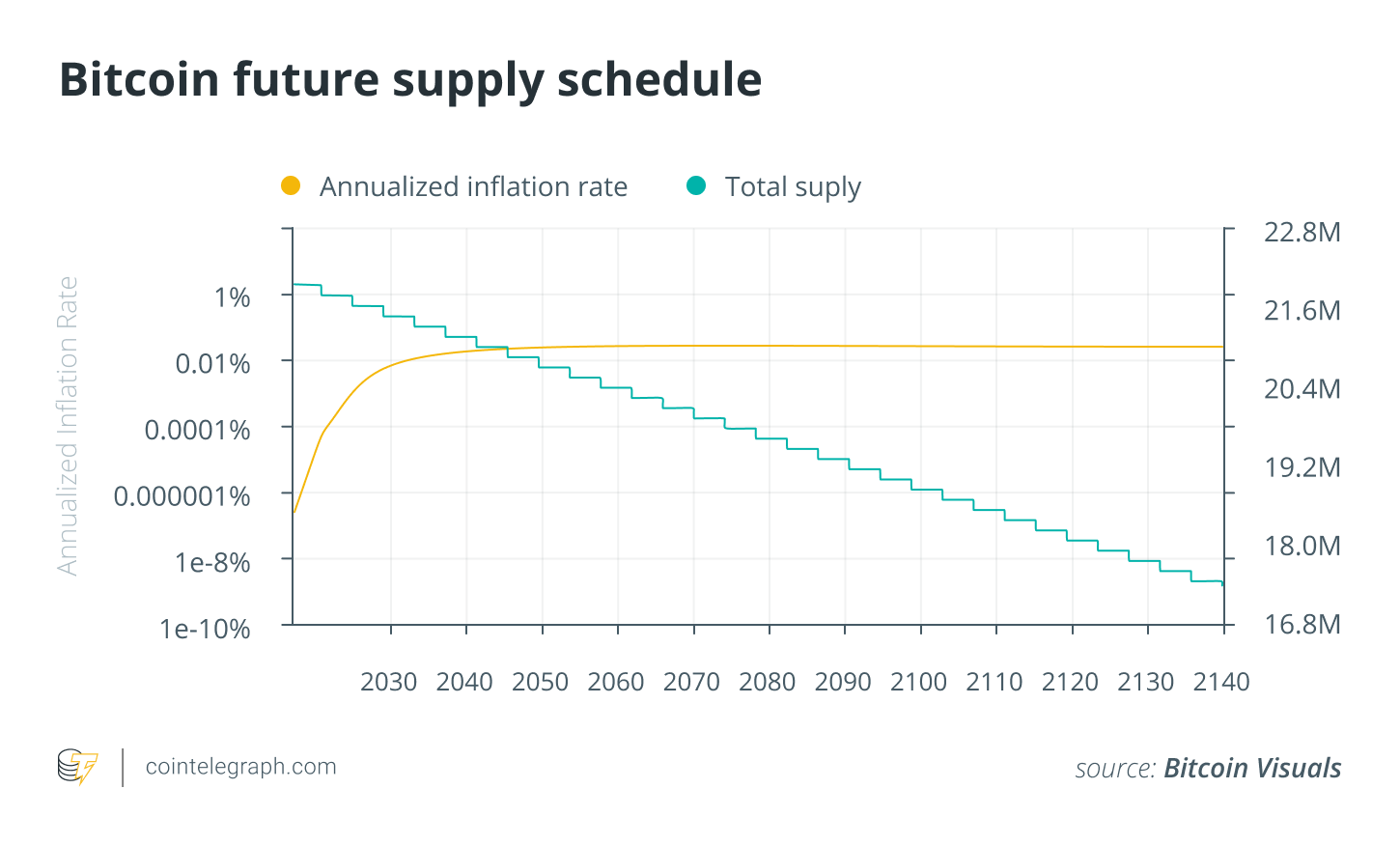

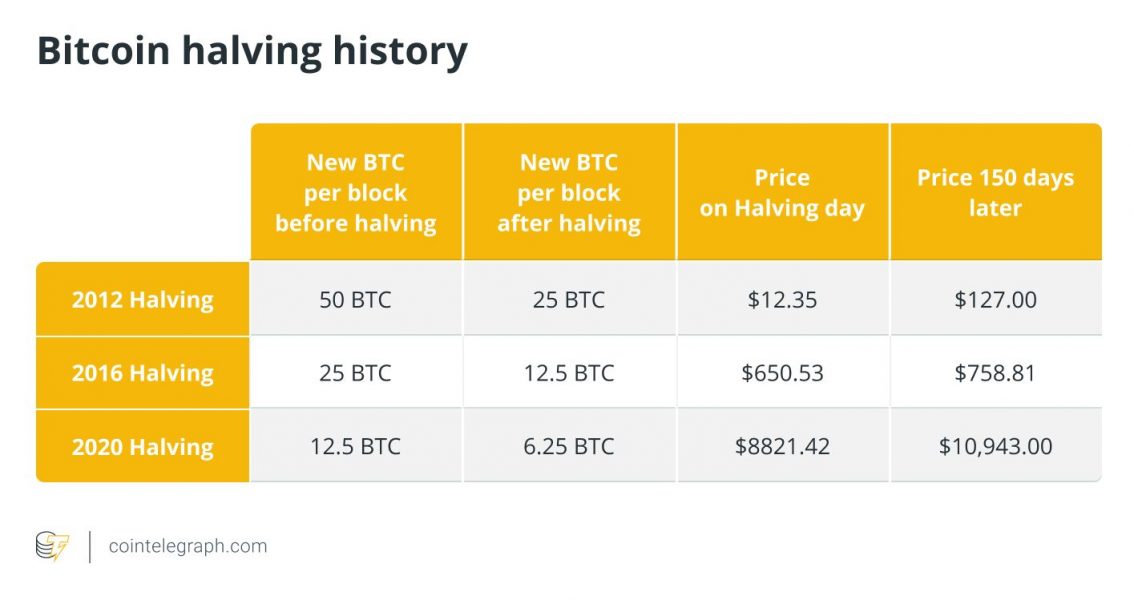

According to Hansen, based on the block discovery rate and the halving process, which occurs roughly every four years — or every 210,000 blocks of transactions — the last BTC will most likely be mined around 2140.

A Bitcoin halving is a planned reduction in the rewards that miners receive, with the next one currently predicted to occur around April 2024. This will reduce the reward for each block to 3.125 BTC or roughly $94,190 at the time of writing.

In theory, by limiting the supply of BTC, each coin’s value should increase as demand increases and supply remains fixed.

Hansen says the price of BTC in 2140 will depend on unpredictable factors such as market demand, the regulatory environment, technological advancements and macroeconomic factors.

“The fact that all Bitcoin is in circulation may create scarcity, but whether this scarcity will translate to price increases is subject to market dynamics,” he said.

“As we look to a future where all Bitcoin has been mined, it’s important to remember that Bitcoin was designed with this endgame in mind.

“The tapering off of block rewards and shift toward transaction fees are intrinsic to the protocol, and represent an ingenious solution to ensuring the ongoing security and viability of the network,” Hansen added.

Jaran Mellerud, a research analyst from Hashrate Index, told Cointelegraph that as Bitcoin adoption and usage grows, transaction fees will drastically increase and become the primary source of revenue for mining firms.

Mellerud said that, by the time the last BTC is issued, the block subsidy will have already been so minuscule that it will not significantly impact the coin supply.

“Due to the huge block space demand relative to the scarce block space supply, transaction fees will have to skyrocket in a future scenario of hyperbitcoinization,” he said, adding:

“If you don’t believe there will be sufficiently high transaction fees in the future to justify the existence of mining, you don’t really believe in Bitcoin.”

What about fiat

By the time the last Bitcoin is mined, Mellerud believes its value won’t be measured in United States dollars or other fiat currencies.

He speculates that by then, fiat money systems will have long since collapsed, and Bitcoin could be the successor, becoming the standard unit of account globally.

“Under such circumstances, the only valid way to measure the purchasing power of Bitcoin is by looking at how much energy a Bitcoin or satoshi can purchase,” Mellerud said.

“Just as we currently measure the purchasing power of the U.S. dollar in energy terms, barrels of oil,” he added.

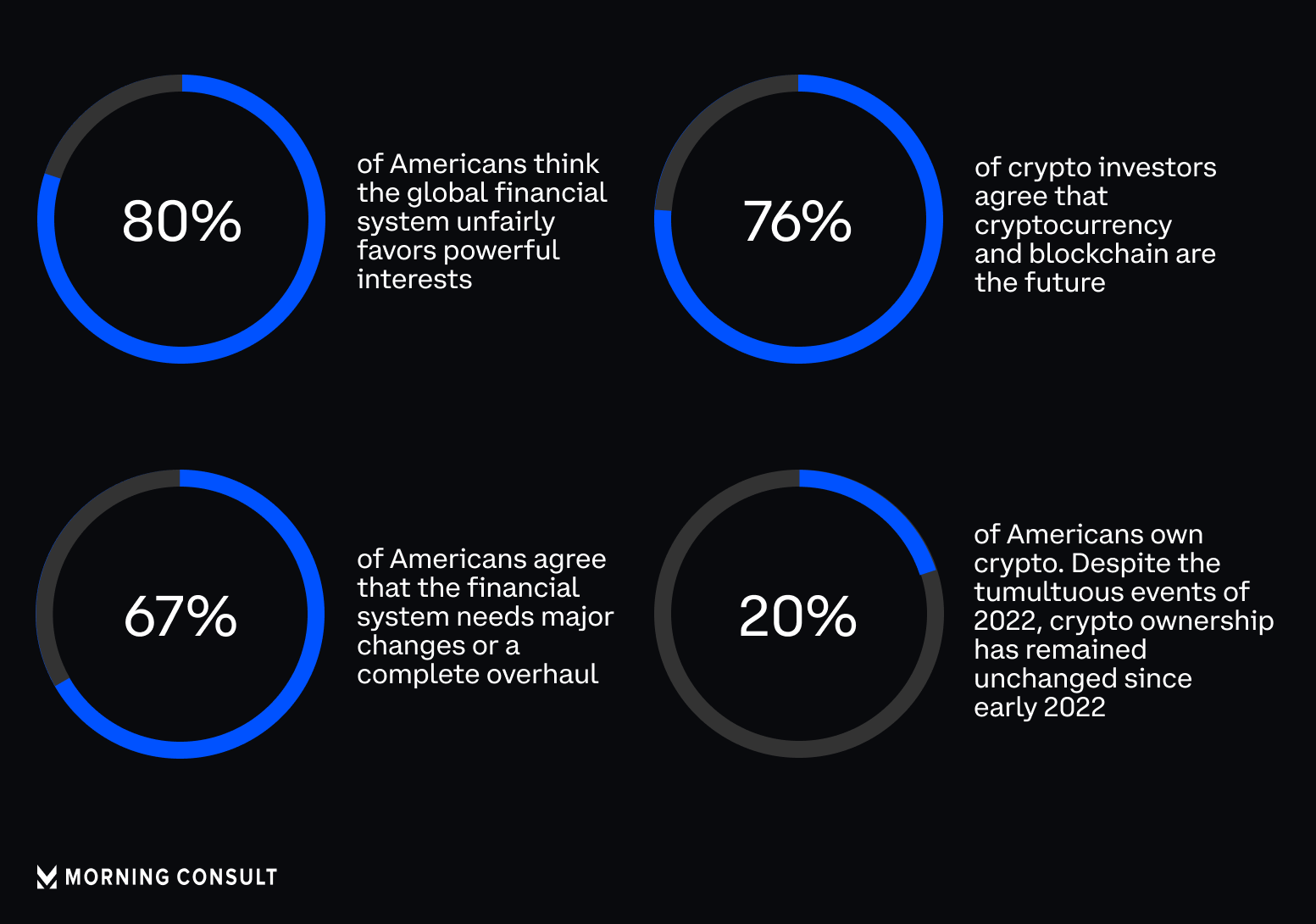

A collapse of fiat money systems has long been predicted, spurred on by the many problems facing the traditional financial system. As recently as March 2023, Silicon Valley Bank collapsed due to a liquidity crisis, with Signature Bank and Silvergate Bank following.

Before the March 2023 banking crisis, a February survey conducted by business intelligence firm Morning Consult and commissioned by crypto exchange Coinbase found most respondents were already disillusioned with the global financial system.

Bitcoin might not be the same in 120 years

Speaking to Cointelegraph, Pat White, co-founder and CEO of digital asset platform Bitwave, believes miners will remain a critical part of the ecosystem, but not all will survive, with some shutting down in the face of mounting costs.

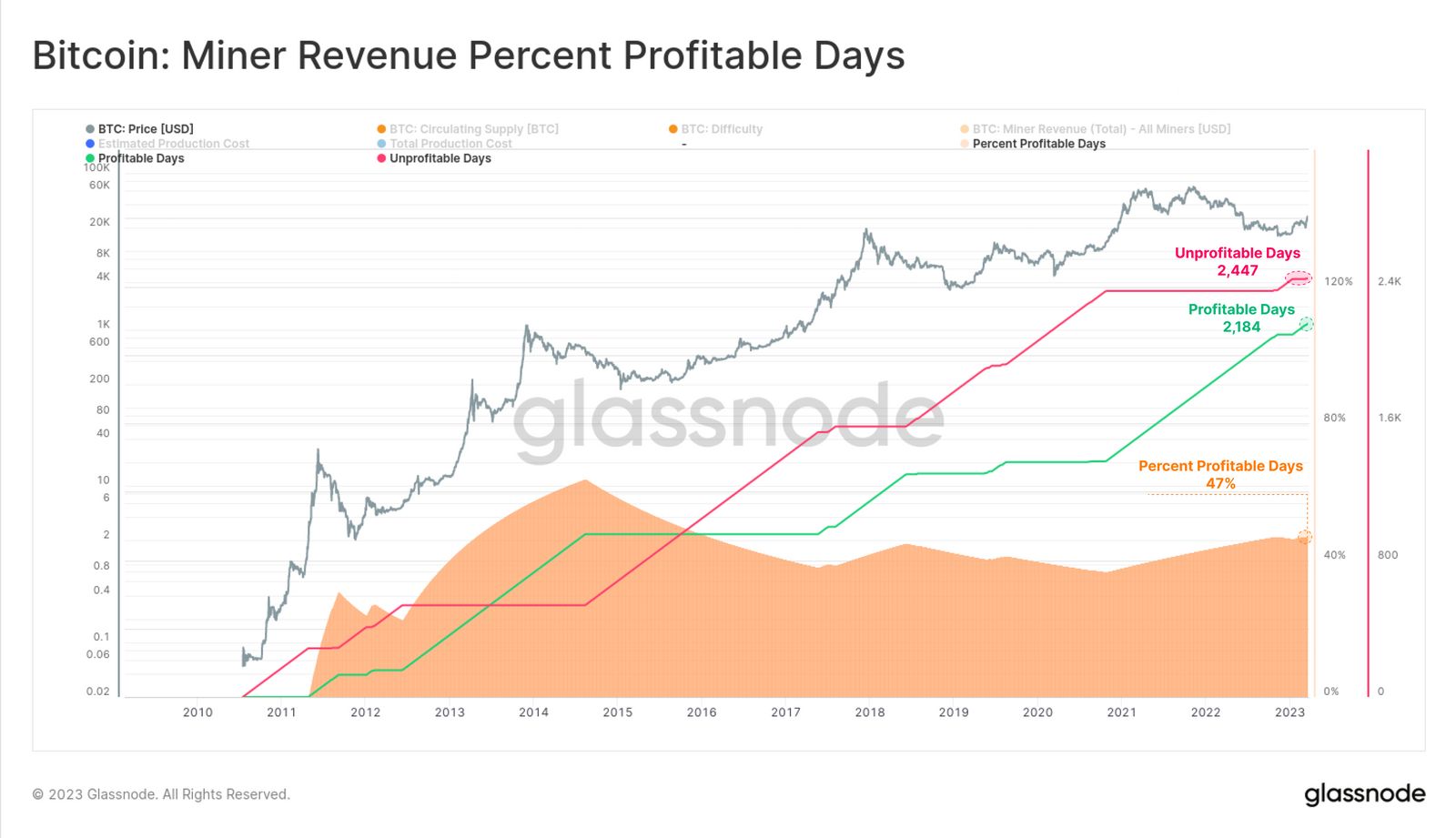

According to a March 24 report from Glassnode, since 2010, miners have already been experiencing long periods of unprofitability, with only 47% of trading days being profitable.

“I think it’s conceivable we’ll see some miners shut down or other manipulation techniques used in an effort to drive up fees,” White said, adding:

“But I also imagine that will happen well before the last Bitcoin is mined since the last few halvings will get the block rewards down to the satoshi level.”

However, White also says “a lot can happen in 120 years,” and BTC could fundamentally change over the next century.

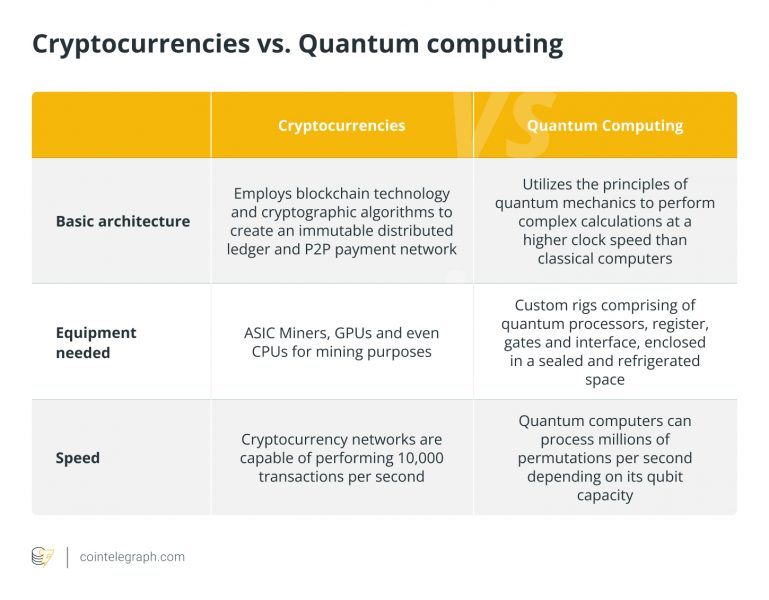

White believes that by 2140, quantum computers will likely have broken the core encryption under Bitcoin, though he says engineers working on it have long known it’s not quantum-secure.

“That shouldn’t necessarily scare people because of this quantum security issue. Between now and 2140, there will have to be a major reworking of Bitcoin from the encryption layer upward,” he said.

“At that point, the Bitcoin developer community will be able to assess whether or not we’re actually on track to have a functioning transaction fee-based network or if additional Bitcoin mining is necessary to ensure the security of the network,” White added.

White further speculates that while Satoshi Nakamoto’s white paper states that 21 million BTC is the supply cap and the single most concrete rule, none of us will likely be alive by 2140 to enforce that rule.

He believes crypto boils down to coding and consensus; if the community thinks the transaction fee incentive is insufficient to keep the network secure, future miners could theoretically extend the BTC hard cap beyond 21 million.

What effect this could have on the price isn’t clear, but either way, White thinks that the price of Bitcoin will stabilize at some global inflation-reflecting price point, and the major price movement will occur at some time in the next 120 years if one or more nations seriously pick it up as their reserve currency.

In that instance, he says it will “likely be independent of Bitcoin mining schedules,” and it would be the most solidifying moment to drive up the price of BTC.

“There are things we can’t even imagine that might impact Bitcoin — wars and energy crises obviously — but what if we’re a true multiplanetary species by then and we have to extend the block production time to support solar system-level communication speeds,” White said.

“What I always find important is to focus on the hardest problems we’re seeing today and do what we can to solve them. That might mean solving for payments or digital ownership, or banking the unbanked — these are the problems to focus on now,” he added.

Source: https://cointelegraph.com/news/the-last-bitcoin-btc-mine