1,272

Views

1,272

Views

0 Comments

0 CommentsWhile interest in crypto has exploded, few people are using it for its intended purpose: to pay for things – writes Tory Newmyer on The Washington Post.

Billionaire tech executive Michael Saylor has called Bitcoin “the seminal invention of the human race.” His website describes it as “a bank in cyberspace” offering a “simple, & secure savings account to billions of people.” He recently claimed ownership of 17,732 Bitcoin worth about $740 million.

But one thing Saylor cannot do with Bitcoin is pay for the $18 shrimp cocktail at Tony and Joe’s Seafood Place several floors below his penthouse apartment on Washington’s Georgetown waterfront. Though Tony and Joe’s has an ATM that can convert cash into Bitcoin, the restaurant won’t accept it.

“I would take Monopoly money before I took cryptocurrency,” said a manager, who declined to give his name.

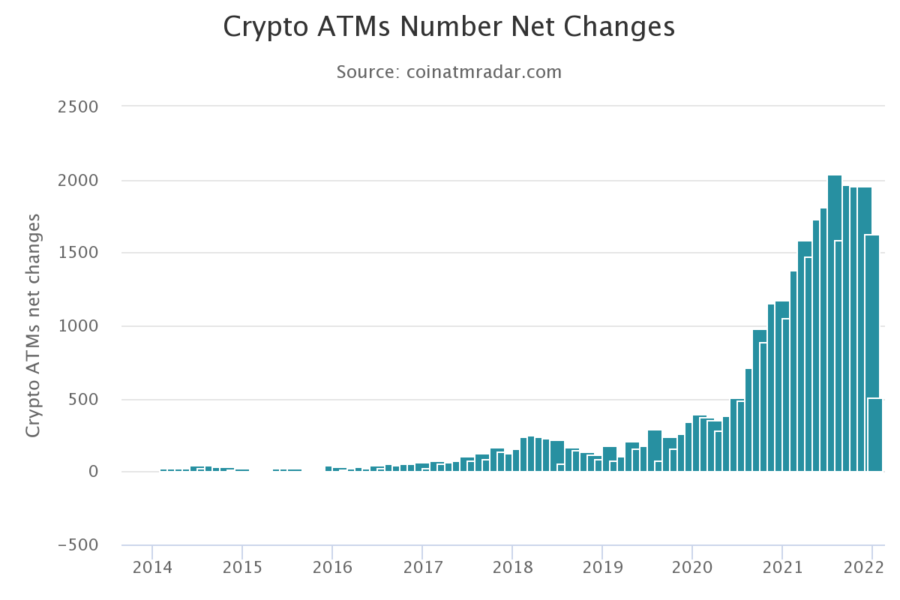

Nearly 30,000 Bitcoin ATMs now dot the American landscape in gas stations, liquor stores and hair salons, up from 1,800 four years ago. About half of Coinstar’s 17,000 kiosks, which convert coins into cash, now sell Bitcoin. And consumers have a growing array of options for buying, selling and transmitting the digital currency, including popular payment apps such as Venmo and Cash App.

Culturally, cryptocurrency is poised for even greater ubiquity: Last month, Staples Center in Los Angeles was renamed Crypto.com Arena in a $700 million deal by the Singapore-based cryptocurrency exchange. The Miami Heat now play in FTX Arena, named for another crypto exchange. And both companies plan to air ads during next month’s Super Bowl, which can draw 100 million viewers.

But for all the hype, there’s scant evidence that digital currencies stand on the threshold of some kind of mainstream breakthrough. While a recent Pew Research Center survey found that 16 percent of Americans have used cryptocurrency in some way, most buy it as a speculative investment, not for its originally intended purpose – as a way to pay for goods and services.

“It’s not happening,” Dan Dolev, a financial technology analyst for Mizuho Securities, said of the notion that crypto is replacing cold hard cash. “I wouldn’t even try to quantify it because it’s so insignificant. People are buying crypto because they think it can only go up. Or because they’ve heard it’s the future. Or because they don’t know why they’re buying it.”

Within Bitcoin, the original and still largest cryptocurrency, only a tenth of transactions amount to any “economically meaningful” activity, according to an October study by the National Bureau of Economic Research. And of that slice, the study concluded traders aiming to buy low and sell high accounted for the vast majority of moves.

For some Bitcoin backers, that’s just fine. Saylor, one of Bitcoin’s most vocal evangelists, declined to comment for this story. But elsewhere, he has said that he views the digital token as an asset akin to gold, meant to be bought and held, not used as an alternative to the dollar.

“You really don’t want to pay for your coffee with your Bitcoin. You want to pay for your coffee with a currency,” Saylor told CoinDesk TV in a recent interview. “I don’t really think it makes sense to pay for things with an appreciating asset. It makes sense to pay for things with a depreciating currency.”

Saylor ranks among the Bitcoin “whales,” a super-rich class of investors who control an outsize portion of the asset. In addition to his personal holdings, Saylor’s company, business software maker MicroStrategy, has plowed its corporate reserves into Bitcoin and borrowed to buy more; it now holds roughly $5.2 billion in the digital currency.

Indeed, the top 10,000 individual investors in Bitcoin own roughly a third of all digital tokens in circulation, the NBER research found, a greater concentration of wealth than exists with dollars among the richest American households. In the second quarter of last year, transactions over $10 million accounted for more than 60 percent of activity in the growing decentralized finance market, the crypto-enabled alternative to traditional financial services, according to a report by Chainalysis.

As the global crypto market has exploded in value – tripling last year from $774 billion to $2.2 trillion, according to CoinMarketCap – it has drawn in a broader swath of the population. The 1 in 6 Americans who report they have invested in, traded or otherwise used cryptocurrency represents a surge from 2015, when only 1 percent reported involvement, according to Pew.

And today’s pool of investors is increasingly diverse. A poll over the summer by NORC at the University of Chicago found that 44 percent of those who bought or traded cryptocurrencies in the past year were non-White, 41 percent were women and 35 percent had annual household incomes of less than $60,000. The survey also found that the average participant was younger than 40 and did not have a college degree.

For some established companies looking to get in on the action, that may be all the evidence they need that there is a future in digital money.

Block CEO Jack Dorsey, the Twitter co-founder who recently quit the social media giant, predicts that Bitcoin will replace the dollar and become the world’s “single currency” within the decade. (Square, which provides e-commerce and banking services to sellers, announced in December it was changing its name to Block.)

Block is acting accordingly, letting people buy and sell the digital currency through its Cash App. The company also is pursuing a number of initiatives focused on expanding the decentralized system Bitcoin is based on, an effort designed to “help Bitcoin reach a mainstream audience,” Dorsey told analysts on the company’s latest earnings call in November.

The push is starting from a modest place. Bitcoin transactions on Cash App have grown over the past two years, the company has said. But fees from crypto transactions made up less than 4 percent of the company’s gross profit in its third quarter. And the volume of Bitcoin transactions on the platform fell by roughly half from the first quarter of the year to the third – a decline that Wolfe Research analyst Darrin Peller attributed to consumers feeling less flush after spending or investing stimulus cash. Bitcoin “has been very slow to be adopted by consumers,” Peller said.

(Source: CoinATMradar )

More options for using crypto in everyday transactions could help. Payment giants Visa and Mastercard both have announced partnerships with crypto firms enabling banks and merchants to offer customers the ability to spend, invest and earn rewards in digital currency. Coinbase, one of the biggest U.S. crypto trading exchanges, now offers a Visa rewards debit card that links users to their accounts on the platform; Crypto.com issues one, too.

But crypto’s path to broader consumer use is hardly traveling a straight line. Major domestic retailers that toyed with accepting Bitcoin through their websites in 2014 – including Dell and Expedia – later abandoned the option when it failed to catch on with customers. Tesla CEO Elon Musk, another billionaire Bitcoin enthusiast, announced last year that the electric carmaker would accept the cryptocurrency as payment. But he reversed himself less than two months later, citing concern over the amount of energy used to mine Bitcoin.

Meta, the parent company of Facebook, has encountered its own challenges to its crypto ambitions. The social media giant sought to become a digital payments juggernaut in 2019, revealing plans to launch a cryptocurrency that would let users exchange money with no transaction fees. But concern among federal regulators that the product could pose risks to the financial system so far has hobbled the project. David Marcus, the executive in charge of it, left the company late last year.

Consumers committed to spending crypto do have options. Overstock, the online furniture retailer, has accepted Bitcoin since 2014. Other major national brands – including AT&T and Regal Cinemas – have partnered with crypto payment processing companies to give their customers that alternative. And some leading charities, including the American Red Cross and the National Kidney Foundation, note on their websites they are now equipped to accept donated crypto.

Block is acting accordingly, letting people buy and sell the digital currency through its Cash App. The company also is pursuing a number of initiatives focused on expanding the decentralized system Bitcoin is based on, an effort designed to “help Bitcoin reach a mainstream audience,” Dorsey told analysts on the company’s latest earnings call in November.

The push is starting from a modest place. Bitcoin transactions on Cash App have grown over the past two years, the company has said. But fees from crypto transactions made up less than 4 percent of the company’s gross profit in its third quarter. And the volume of Bitcoin transactions on the platform fell by roughly half from the first quarter of the year to the third – a decline that Wolfe Research analyst Darrin Peller attributed to consumers feeling less flush after spending or investing stimulus cash. Bitcoin “has been very slow to be adopted by consumers,” Peller said.

More options for using crypto in everyday transactions could help. Payment giants Visa and Mastercard both have announced partnerships with crypto firms enabling banks and merchants to offer customers the ability to spend, invest and earn rewards in digital currency. Coinbase, one of the biggest U.S. crypto trading exchanges, now offers a Visa rewards debit card that links users to their accounts on the platform; Crypto.com issues one, too.

But crypto’s path to broader consumer use is hardly traveling a straight line. Major domestic retailers that toyed with accepting Bitcoin through their websites in 2014 – including Dell and Expedia – later abandoned the option when it failed to catch on with customers. Tesla CEO Elon Musk, another billionaire Bitcoin enthusiast, announced last year that the electric carmaker would accept the cryptocurrency as payment. But he reversed himself less than two months later, citing concern over the amount of energy used to mine Bitcoin.

Meta, the parent company of Facebook, has encountered its own challenges to its crypto ambitions. The social media giant sought to become a digital payments juggernaut in 2019, revealing plans to launch a cryptocurrency that would let users exchange money with no transaction fees. But concern among federal regulators that the product could pose risks to the financial system so far has hobbled the project. David Marcus, the executive in charge of it, left the company late last year.

Consumers committed to spending crypto do have options. Overstock, the online furniture retailer, has accepted Bitcoin since 2014. Other major national brands – including AT&T and Regal Cinemas – have partnered with crypto payment processing companies to give their customers that alternative. And some leading charities, including the American Red Cross and the National Kidney Foundation, note on their websites they are now equipped to accept donated crypto.

Small businesses have been slower to follow suit. At Reiter’s Books, an independent bookstore across from the World Bank in downtown Washington, customers can browse titles on blockchain technology on the shelves and convert cash into Bitcoin at the shop’s ATM. But owner Robert Nelson doesn’t accept crypto as payment. And he says a customer has yet to use the crypto option on the ATM, which is owned and operated by a vendor who gives him a cut of the transactions. “The whole thing is baffling,” Nelson said.

Even as crypto’s practical value remains in question, its huge gains as an investment asset have proved irresistible, even to some typically risk-wary investors.

In October, the Houston Firefighters’ Relief and Retirement Fund said it bought $25 million in Bitcoin and ether, the second-most popular cryptocurrency. And two funds for workers in Virginia’s largest county likewise are taking the plunge: The Fairfax County Police Officers Retirement System and the Fairfax County Employees’ Retirement System are investing a total of $50 million in a Parataxis Capital Management fund, which buys digital currencies and crypto derivatives.

Elsewhere, top asset managers BlackRock, Fidelity and Vanguard are investing in Bitcoin mining, the energy-intensive computing networks critical to validating transactions on the decentralized network. And while Fidelity and Vanguard have yet to allow workers saving for retirement to invest their 401(k) funds in crypto, the industry could be headed that way: Over the summer, ForUsAll, a small 401(k) provider, announced a partnership with Coinbase that allows plan participants to invest up to 5 percent of their retirement funds in digital currencies.

The moves have raised alarm among some academics who study crypto.

“My view is that crypto might be appropriate for some retail investors but certainly not all,” said Sarah Hammer, senior director of the Harris Family Alternative Investments Program at the University of Pennsylvania’s Wharton School. “A fundamental principle of investing is that, as you approach retirement, your portfolio should be less and less volatile, so you can rely on it for retirement income. So it behooves folks to be cautious.”

An ongoing sell-off in top cryptocurrencies demonstrates the point. Bitcoin is down about 40 percent since reaching an all-time peak of about $69,000 two months ago; Ether has dropped the same magnitude over that period. Bitcoin has a track record of such volatility; last year, its price fell by half from March to July before rallying into the fall.

The industry itself, awash in newly minted wealth, is spending heavily to promote the idea that crypto is a safe bet, enlisting a series of celebrities to tape TV ads encouraging viewers to invest. Among them: Tampa Bay quarterback Tom Brady, who in September told the SiriusXM podcast “Let’s Go” that he’d “love to” receive a portion of his NFL salary “in some Bitcoin or Ethereum or Solana tokens.”

But an ad for Crypto.com featuring actor Matt Damon sends a slightly different message. After extolling a series of adventurers throughout history as “the ones who embrace the moment and commit,” Damon gazes off at a scary-looking red planet in outer space.

“Fortune,” he says, “favors the brave.”